Scenarios and obstacles

Extraterrestrial resources myth and reality

From the south pole of the moon to the asteroid 16 psyche, the prospect of using extraterrestrial resources is transforming space exploration into a new arena of technological, economic and legal competition

14 minFor much of the history of space exploration—which began with the launch of the first artificial satellite, Sputnik 1, by the Soviet Union on 4 October 1957—space has been perceived primarily as a symbolic and political domain. The competition between the two superpowers of the time, the Soviet Union and the United States, to achieve firsts in space—culminating in sending the first humans, American astronauts Neil Armstrong and Buzz Aldrin, to the Moon—was first and foremost a technological challenge, but also a way for one of the two powers to assert its political and scientific leadership to the world.

Beyond serving as the arena for ideological competition during the Cold War, space has been a laboratory for international scientific cooperation. Technologies that were then in their infancy have now reached a high degree of maturity—at least some have, such as satellite telecommunications, Earth Observation, and precision navigation and geolocation systems. This progress has opened up a real market, with services and applications that can benefit citizens in every country, including emerging and developing nations, even where they have no space assets of their own.

Consequently, the objectives of space activities have changed—or, more precisely, expanded—and with them the narrative that accompanies them. Space is no longer merely a field of competition or scientific exploration: it has become a critical infrastructure for Earth.

Our digital economies are increasingly dependent on satellite services: telecommunications, navigation, Earth Observation, climate monitoring and national security. In this context, a new strategic question arises: can space also become a source of material resources?

The prospect of exploiting extraterrestrial resources—metal-rich asteroids or lunar ice usable as fuel—is often presented as the next “gold rush,” though I have my own doubts about that framing. The reality is that we are indeed at the dawn of a large-scale space mining industry, and thus in the early stages of building a new economic, technological and legal ecosystem. The systematic exploration of the solar system is becoming everyone’s business, and the race is resuming, for reasons even more complex than those that drove the start of the space age, because technological and political supremacy are now joined by geopolitical—or rather, astro-political—considerations, with a potential impact on planetary governance and consequences that are not always predictable. But let’s see why.

What resources? Reality and strategic narrative

When it comes to space resources, the collective imagination tends to focus on asteroids rich in precious metals. In reality, in the medium term, the most significant resources may be found on other celestial bodies, starting with the Moon. It is close to Earth and possesses potentially valuable resources, such as water, helium-3 and rare earth elements. Furthermore, its south pole—located on the side not visible from Earth—features areas that are almost constantly illuminated. Wouldn’t this therefore seem the ideal place to set up a base and begin mining operations? Unfortunately, the reality is more complex. As we shall see, the area is dotted with craters, where landing is limited almost exclusively to the rims. The truly usable sites are very few, and that is precisely why a race to be first is bound to begin.

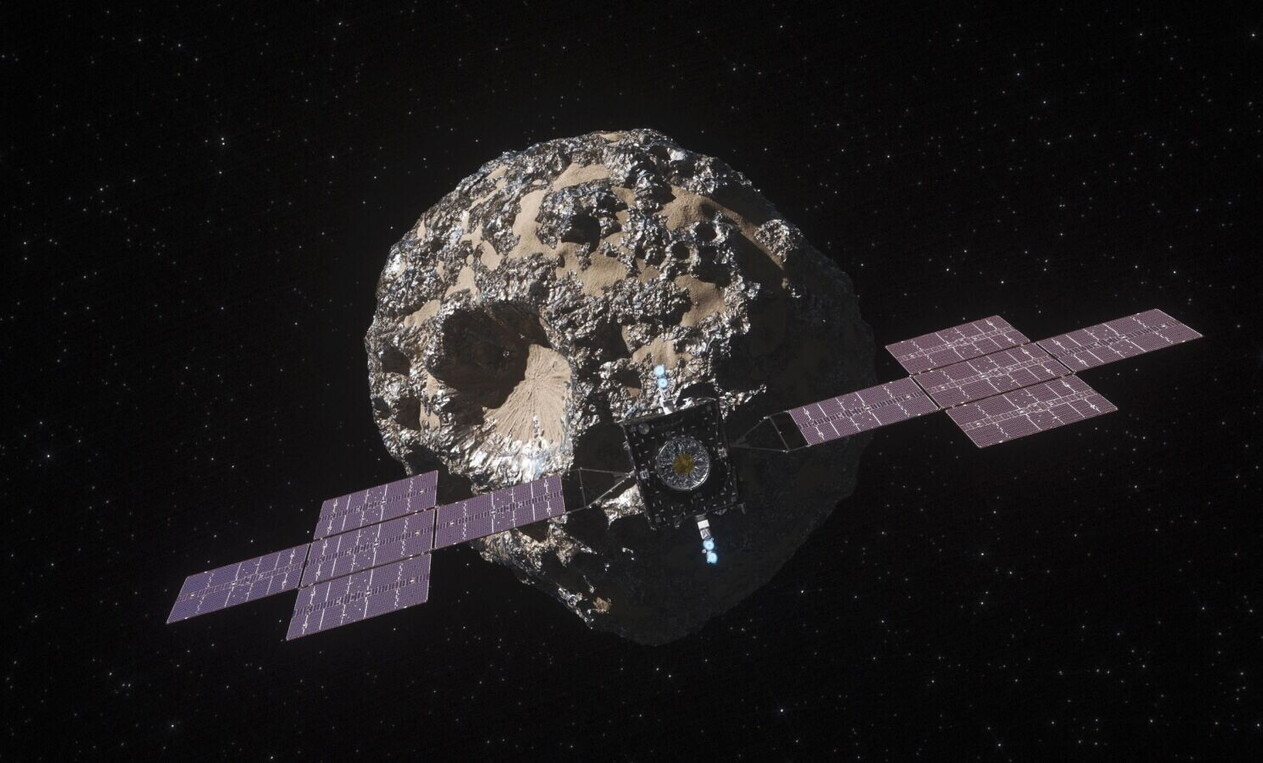

Asteroids, particularly metallic ones, contain iron, nickel and platinum group metals. The best-known example is 16 Psyche, the subject of NASA’s mission of the same name. It has an average diameter of around 220 km and is considered one of the most metal-rich bodies in the main belt, the asteroid-crowded region of the solar system between Mars and Jupiter. Some popular estimates attribute a theoretical value of over 10,000 quadrillion dollars to its metal resources. With the necessary technologies and an internationally agreed regulatory framework, what would happen if even just a fraction of these metals and rare earth elements were brought back to Earth? How would the balance of power on Earth shift around rare earth elements, which are so crucial to cutting-edge technologies such as artificial intelligence and digital cooperation? We are beginning to glimpse how the space economy and astropolitics will play an increasingly decisive role in geopolitics on Earth.

Programs and actors: cooperation and competition

The United States has revived lunar exploration with the NASA-led Artemis program. In support of this, the Artemis Accords represent a bottom-up attempt to define operational principles for the use of space resources, and more.

Over sixty countries have joined the accords and wish to collaborate with NASA in this sector. Private players such as SpaceX and Blue Origin are also coming to the fore, intending to play a leading role in the Artemis exploration program, with their own ambitions reaching toward Mars and beyond.

China, through the China National Space Administration (CNSA), is promoting the International Lunar Research Station (ILRS). Here too, over ten countries have joined the relevant agreements, alongside international organizations and the private sector. Meanwhile, China is continuing its Chang’e missions, preparing for a more systematic presence on the Moon and, wherever possible, bringing samples back to Earth. Europe, through the ESA, maintains a multilateral approach.

However, as already mentioned, everyone is targeting the Moon’s south pole. Not forgetting India, which in August 2023 landed the Chandrayaan-3 mission right in the middle of a summit held by BRICS—the group comprising Brazil, Russia, India, China and South Africa—showcasing its technological capabilities to the world and, in effect, staking its claim at the table of global decision-makers. History, in a sense, is repeating itself.

Of course, we are talking about extremely complex space missions. Reaching another body in the solar system, landing, extracting resources and transporting them to Earth requires highly advanced technological capabilities. Robotics, extraction technologies, transport systems, and launch window management: these are all factors that significantly affect the costs and economic viability of operations which, at least on paper, could have a huge impact.

However, there is also the “space for space” perspective—extracting and using resources directly on site, without the need to bring them back to Earth. If a human outpost were to be established on the Moon, for example, the use of locally available resources—such as water—would avoid the need to transport them from our planet, making the stay of a handful of Earthlings far less complex and decidedly more resilient.

The economy of extraterrestrial resources

With around 80 countries currently pursuing structured plans for solar system exploration, with growing industrial interest in resource exploitation given the economic stakes at play, and with the technological challenges in the process of being resolved, what is the short-term outlook between now and 2030?

The size of the asteroid mining market alone reached USD 2.10 billion in 2024 and is likely to exceed USD 11 billion by 2032 (see the chart above). Forecasts, of course, can lead to conclusions that are not entirely accurate, but they nevertheless help us understand the trend. Between 2024 and 2032, the market is expected to grow at a compound annual growth rate (CAGR) of around 24 percent, driven primarily by the prospects for using the extracted resources and by a growing concentration of private capital. This signals an increasingly strong commercial interest in this emerging sector.

On the other hand, even if we treat the valuation of asteroid 16 Psyche as overestimated, we are still faced with a potential revolution—perhaps not imminent, but already creeping in. If we take the latest global GDP figure—approximately USD 111 trillion—as a reference, the theoretical value attributed to this metallic asteroid—estimated at around USD 10,000 quadrillion—would be roughly 90,000 times greater than the planet’s entire annual economic output. This is, however, a purely theoretical figure, one that does not correspond to any economic value that could actually be realized; it derives from an estimate of the quantity of metals contained in the celestial body multiplied by current Earth prices for raw materials. Even if we accept that this value is not fully attainable, it is difficult not to grasp the potential impact that such a prospect could have on the planet, from a social, political and economic perspective.

The issue of international law

The use of extraterrestrial resources has gradually emerged as one of the most sensitive matters in defining the future governance of space. The main multilateral forum in which this debate takes place remains the United Nations Committee on the Peaceful Uses of Outer Space (COPUOS), supported by the United Nations Office for Outer Space Affairs (UNOOSA), which for over sixty years has been at the heart of space diplomacy and the development of international space law. The reference framework remains the 1967 Outer Space Treaty, which establishes the fundamental principle of non-appropriation and affirms that the exploration and use of space must be for the benefit of all humanity.

However, the treaty was conceived at a time when economic activities in space were still far removed from today’s technological and industrial reality. Precisely to fill this gap in interpretation, in 2021 the COPUOS Legal Subcommittee established a Working Group on Legal Aspects of Space Resource Activities, with a multi-year work program extending through 2027, tasked with examining the legal implications of resource exploitation activities and identifying possible elements of a future shared regulatory framework. The WG has been greatly inspired by grassroots initiatives originating from a range of stakeholders, such as The Hague International Space Resources Governance Working Group, which between 2016 and 2019 developed what are known as the “Building Blocks for the Development of an International Framework on Space Resource Activities,” a set of principles and potential regulatory instruments designed to guide the development of a future international regime. Among the issues addressed are the role of states in authorizing private activities, the registration and transparency of operations, the establishment of safety zones to prevent interference between operators, the protection of the space environment, and the sharing of benefits derived from the use of resources. The results of this WG were subsequently brought to the attention of COPUOS, ensuring they were addressed through the proper channels. Another example of this kind is the Artemis Accords, which explicitly recognize the possibility of using space resources in accordance with international law and introduce operational concepts such as safety zones, with the aim of promoting cooperation and transparency in lunar activities.

Taken together, these two strands—the UN’s multilateral process on the one hand, and the conceptual work developed by the Hague group and operational initiatives such as the Artemis Accords on the other—reflect the emergence of a new phase in space governance, in which the evolution of the space economy requires an increasingly complex balance between technological innovation, national interests and collective responsibility towards a domain that continues to be regarded as the common heritage of humanity.

Possible future scenarios (2025-2045)

So, what will happen? It is difficult to predict. There are three plausible scenarios: regulated cooperation, fragmented competition, or an economic slowdown in the space mining industry. Given the impetus coming from the private sector, I do not believe a slowdown is possible. COPUOS will do its job, UN member states will agree on a number of guidelines, and the private sector and space agencies will continue to develop technologies for the near future, including for long interplanetary journeys or installations on other bodies in the solar system, so they can survive with little or no material brought from Earth. In the medium term, I see a likely combination of selective cooperation and strategic competition, alongside a potentially booming market.